GST being a tax arising on supply of goods and/or services, helms the indirect taxation scenario of the country. While transactions amounting to supply of both goods and services are covered under GST, there is a vast difference between the tax rates, place of supply, time of supply, time of invoicing; between supply of goods and that of services. The primary reason for the differentiation essentially lies in the ‘form/nature of existence’ of goods and services.

Eway bill

Goods are movable and tangible whereas services are intangible, hence the concept of movability does not apply to them. When the goods are movable, in most cases the ‘supply’ of such goods from one person to another would involve their movement from one location to another- intra-state, interstate or crossing national boundaries. Presence of physical movement may lead to numerous tax evasion practices indulged into by fraudulent taxpayers. In a major effort to curb such illegal or unauthorised movement of goods, GST Act has made it mandatory for the person in charge of the conveyance to carry with him an ‘e-way bill’ as a necessary document without which the movement of goods would be treated as unauthorised and attract penal provisions under the law. ‘Electronic way bill’ or ‘E-way bill’ is a document prescribed under the GST law to be generated on the designated common portal i.e. https://ewaybillgst.gov.in. E-way bill is a document to be necessarily generated by a registered person when there is a movement of goods of consignment value exceeding fifty thousand rupees, if not expressly exempted under the regulatory rules. Section 68 of the CGST Act 2017 which deals with the inspection of goods in movement requires the person in charge of a conveyance carrying any consignment of goods to carry along with him prescribed documents and devices. Rule 138 of CGST Rules 2017 is the corresponding rule which prescribes the document mentioned under Section 68 of the Act to be the ‘E-way bill’.

GST E-Way Bill

However, the relevant base document i.e. the invoice, bill of supply, bill of entry (in case of imported goods) or the delivery challan would have to be carried along by the person-in-charge of the conveyance.

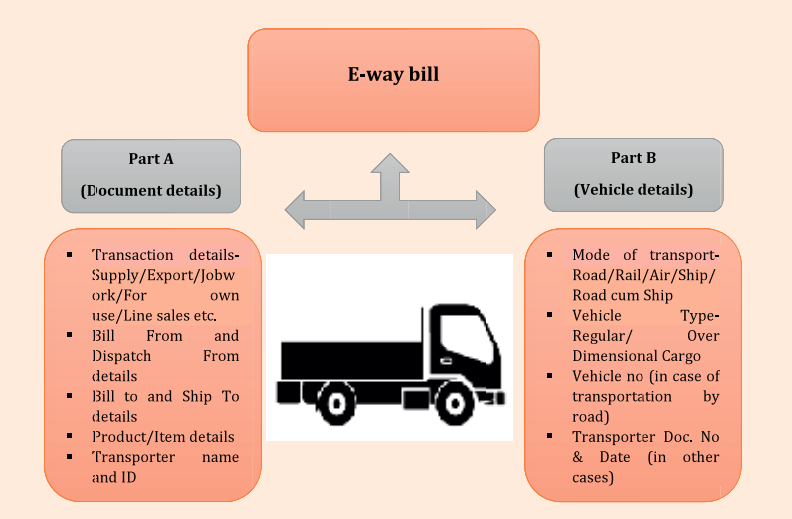

What Consititutes an E-Way Bill?

E-way bill being a document to be carried along with the goods that are transited through a conveyance, it is obvious to include the details of such goods being transported. E-way bill is a document supplementary to the other fundamental documents prescribed under the Act i.e. tax invoice, credit or debit note, delivery challan, etc. Thus, whenever a tax invoice (for supply of goods) or delivery challan (for reasons other than supply) is issued, Part A of the e-way bill consisting of the invoice/challan details is supposed to be furnished. On filling of relevant details in Part A, a unique temporary number is generated. Part A of the e-way bill consists of the document details such as the supplier name, GSTIN and address, the recipient details, invoice number and invoice date, description and HSN of goods. However, e-way bill is generated only after filling vehicle details in Part B. On successful reporting of details in Part B, a valid e-way bill for movement of specified goods comes into existence.

Who can generate an E-Way Bill?

PART A OF E-WAY BILL:

Part A of the E-way bill is required to be generated prior to movement of goods and can be generated either by:

Registered person (either the supplier or recipient) causing movement of goods ORTransporter, on an authorisation from the registered person ORE commerce operator or courier agency, on an authorisation from the registered person

In cases where the transporter is not a registered person under GST, he may enroll on the e-way bill portal to get 15 digit unique transporter ID (TRANSIN). The clients may then enter this number in Part A of e-way bill for assigning goods for transportation. Information furnished in Part A of e-way bill is made available to the registered person to utilise the same in GSTR 1.

PART B OF E-WAY BILL:

Part B of the E-way bill with vehicle details can be generated by:

In case of transportation by owned conveyance/ hired/public conveyanceBy the registered person being a supplier or a recipientIn case of transportation by railways/air/vessel – By the registered person being a supplier or a recipientTransporter, in cases where goods handed over to him for transportation

Validity of E-Way Bill

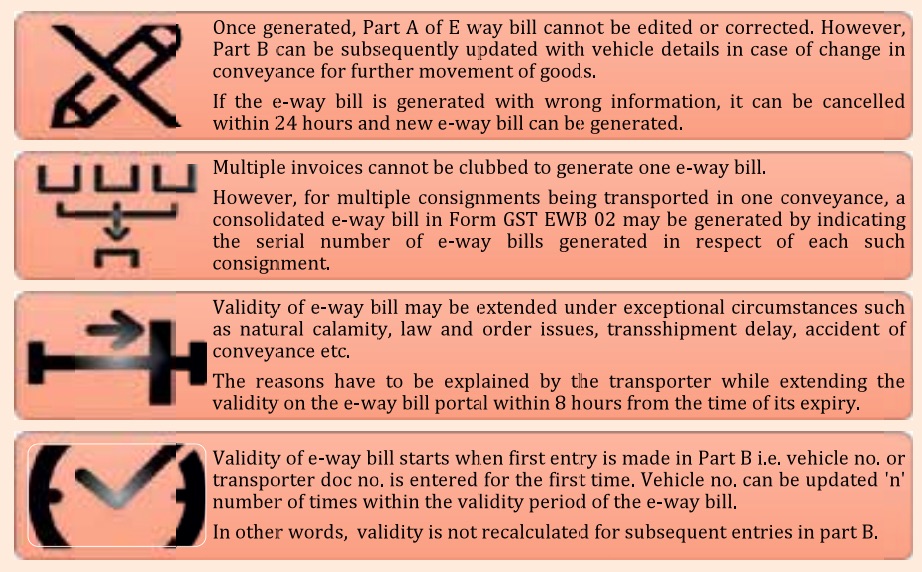

Noteworthy Points:

Restriction on Furnishing of Information In Part A of E-Way Bill:

No person shall be allowed to furnish the information in Part-A of Form GST EWB-01 when:

He has not furnished the statement in Form GST CMP08 for two consecutive quarters (being a composition scheme taxpayer)He has not furnished the GSTR 3B returns for a consecutive period of two months (being a regular taxpayer)He has not furnished the GSTR 1 returns for any two consecutive months or quarters, as the case may be.

The concept of e-way bill has revolutionised movement of goods to a considerable extent. Further, there are regular enhancements being made in the practical modalities on the e-way bill portal. For e.g. e-way bill cannot be generated with only SAC codes (99) for services, minimum one HSN code belonging to goods is mandatory. Based on the principle of self-reporting, e-way bill compliances ensure faster movement of goods without unnecessary detention of vehicles. There is objective checking of vehicles done by the officers that aids in detection of recycling, bill trading and other frauds. Being practically implemented since April 2018, e-way bills have completed 3 years of operationalization and undeniably has been one of the key highlights of the GST system. Official Website Recommended Articles

E-way LoginE-way RegistrationGST Council approves E-Way BillGST E-Way Bill RulesOverview of the provisions of e-way billArticle on E-Way Bill under GSTE-Waybill under GSTGST Council approves E-WayFeatures of the e-Way Bill SystemPoints to be noted about E-way Bill