Form 26AS is an important document that plays a big role in your Income-tax filing process. It is the document that you refer to verify and pick information to file your income tax return. This form is also known as the Tax Passbook or the Annual Tax Statement. It includes all information regarding Tax Deducted at Source (TDS) on your salary, other income, interest received from the bank, demands, refunds, etc. If you like this article then please like us on Facebook so that you can get our updates in future ……….and subscribe to our mailing list ” freely “

What is form 26AS :

Form 26AS is a consolidated tax statement issued under Rule 31 AB of Income Tax Rules to PAN holders. It contains the details about how much of one’s tax has been received by the government and is consolidated from all the related sources like salary, pension, interest income, etc., This statement is issued with respect to a financial year. It consists of details regarding the following :

(1) Tax deducted at source (TDS)(2) Tax collected at source (TCS)(3) Advance tax / self-assessment tax / regular assessment tax etc. deposited in the bank by the taxpayers (PAN holders).(4) Refund received during the financial year.

Changes in the New Form 26 AS 2020

The New Form is divided into 2 parts – one is Part A& another is Part B, where Part A will show all the personal details and Part B is all about your tax deductions, specified financial transactions, tax paid, penalties, pending or completed proceedings, etc.

Changes in Part A – Personal Details

The earlier form captured details such as your full name, PAN number and your address. The new form will include additional details such as your date of birth/incorporation (for companies/ partnerships/Sole proprietors), Aadhaar number, mobile and email address as well. Inclusion of these details will help you verify if all your details with the Income Tax dept and other agencies where you conduct financial transactions are the same, and get them corrected, if necessary.

Changes in Part B – Financial Details

The New format of 26AS will consist of following information:

Information related to TDS/TCS

This section formed the cornerstone of the earlier Form 26 AS. This section continues to show all transactions where tax has been deducted and deposited against your PAN.

Information related to Specified Financial transactions (SFT)

This section is a fresh addition to Form 26AS. All the transactions like:

- Investments in mutual funds, equities, corporate bonds or debentures,2. Sale or purchase of immovable property (real estate)3. Foreign currency transactions4. Cash deposit or withdrawal from an account,5. Cash payment for bank drafts6. Payment of credit card bills or for any goods or services in cash/electronic means or7. Buyback of shares above a certain limit

will be recorded in the Form. The changes in this section are done to encourage transparency in tax filing and avoid instances of non-reporting and tax evasion.

Information related to taxes payment

The old form 26AS consist of details of taxes deducted and collected from you, along with the details of taxes paid by you, the new form will also have advance tax or self-assessment tax. This addition will help you to verify whether your employer/ bank/ payer of the tax has in fact deposited the tax with the government. And if not, then you can take proper action regarding this.

Information related to demand and refund

Once you file your tax return, it is assessed by the Income Tax officials to see if you have paid the taxes in tune with the existing rules and regulations. If there is any extra tax to be paid, you would be intimated in the form of a demand. This type of information will help you to verify whether the same demand is genuinely outstanding or disputed.

Information related to pending and completed tax proceedings

The new form will show you details of all the pending tax proceedings and details of completed tax proceedings, against your PAN.

Importance :

(1) This form 26AS is required to be cross checked with the details in form 16 and 16A to confirm that

(a)The tax deducted or collected by the Deductor / Collector has been deposited to the account of the government.(b) The Deductor or Collector has accurately filed the TDS / TCS return giving details of the tax deducted/collected on your behalf.(c) Bank has properly furnished the details of the tax deposited by you.

Reason of Difference between Actual TDS & TDS Reflected in Form 26AS

In case of difference between actual TDS and stated TDS, the taxpayer cannot claim the actual amount of TDS due To the Following reasons-

Non-compliance of details to the departmentIncorrect account numberWrongly file TDS RETURNLATE DEPOSITION OF TDSOmission in return

NOTE– In this case, the taxpayer should approach the deductor and request him to take the necessary steps.

How to verify the details in Form 26 AS :

Form 26AS is divided into Part A, B and C, D ,E,F. They are :

(1) Part – A : Details of Tax Deducted at Source

It contains the details of tax that has been deducted at source (TDS) by each deductor who made a specified kind of payment to the assessee. Section under which the deductor is categorized-

on salary under section 192,interest income u/s 194A and 193dividend income u/s 194 and 194Dprofessional services U/S 194J ,Work contract services U/S 194C andPrize winnings U/S 194B

Details to be mentioned-

Name & TAN of deductorThe total amount paid/creditedAmount of TDS deducted and deposited Section under which it has been deducted Date from which the payment has been effected Date of credit/payment etc.,

and date of the e-transaction and date of booking also mentioned and the Information is provided on a Quarterly Basis. Status of booking tax- It refers to the status of tax transactions and could be referred to by symbols like U- Unmatched, P- Provisional, F-Final, and O- Overbooked.

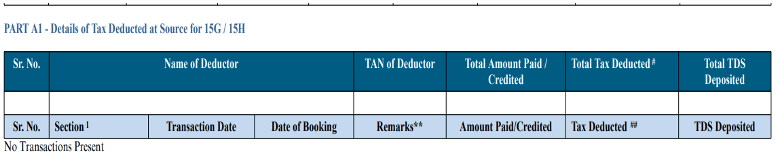

Part A1: Details of TAX deducted at source FROM 15G/15H

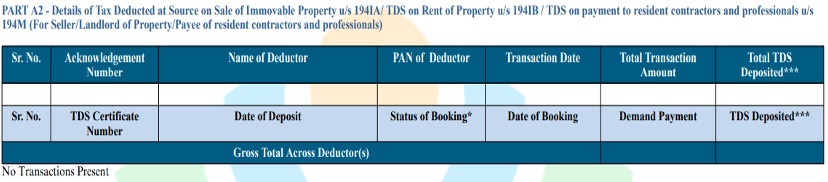

There may be some reason when your earned income is less than exempt income but you have income from FDR or other saving scheme , in this case to avoid TDS , one is required to submit FORM 15G ( AGE <60 YEARS) OR FORM 15H (AGE 60> YEAR) with the bank. Once the information is submitted through FORM 15G OR FORM 15H, you are exempted from paying TDS AND these details will reflect in part A1 OF form 26as. Details to be mentioned: Along with this TAN of Deductor, Total amount paid/credited, Amount of TDS deducted and deposited and date of the transaction and date of booking also mentioned And the Information is provided on Quarterly Basis. PART A2: Details of TDS on sale of immovable property, TDS on rent of property, TDS on payment to resident contactor (for seller/landlord of property/payee of resident contractors and professionals) As per section 194IA of the income tax act, the buyer is required to deduct tax @ 1% of the amount paid /credited to the seller and as per section 194 IB OF INCOME TAX ACT, Individual /HUF not required to get his account audited paying rent more than 50,000 per month is required to deduct TDS @5 % from the payments and as per section 194M of income tax act, Individual/HUF not required to get his account audited paying amount for carrying out any contractual work or professionals service in a financial year exceed 50,00,000 required to deduct TDS @ 5%. Now this details will be available in form 26as so that deductor can verify the amount form here. This credit is available for claim in ITR by the seller.

(2) Part – B : Details of TAX collected at source

Part B of form 26as shows details of TCS I.E. Tax collected at source in case of an individual who is a seller and collecting tax the details of TCS will be shown in PART B. Along with this TAN of Collector, Total amount paid/credited, Amount of tax collected, and TCS deposited and date of the transaction and date of booking also mentioned. It contains the details of tax collected at source (TCS) by the seller of specified goods (such as Alcoholic liquor for human consumption, Scrap, Parking lot, Toll plaza) at the time these goods have been sold to the assessee. It consists of the details as said in part A but of the person who has collected the Tax.

(3) Part – C :Details of tax paid (other than TDS AND TCS)

If any tax is deposited by self like advance tax, self-assessment tax will be present here. Along with this it also has details of challan through which tax deposited. Thus part shows the details of income tax directly paid by the assessee, like advance tax, self assessment tax, and details of the challan through which tax has been deposited in the bank.

(4) Part – D : Details of Paid Refund

If any refund is received that information will be present here along with the assessment year to which refund relates along with mod of payment, nature of refund, the amount of refund paid and interest paid and also the date of payment is mentioned here.

(5) Part – E : Details of SFT Transaction

Part E of form 26as will show specified financial transactions from a specified person like banks, mutual funds, institutions issuing bonds and registrar OR sub-registrar, etc. under section 285BA of the income tax act 1961. The due date of filing the statement for the financial transaction is 31st May of immediately following the financial year in which the transaction is registered.

(F) PART F:

Details of TDS on sale of immovable property, TDS on rent of the property, TDS on payment to the resident contractor (for buyer/tenant property/payer of resident contractors and professionals) As per section 194IA of the income tax act, the buyer is required to deduct tax @ 1% of the amount paid /credited to the seller and as per section 194 IB OF INCOME TAX ACT, Individual/HUF not required to get his account audited paying rent more than 50,000 per month is required to deduct TDS @5 % from the payments and as per section 194M of the income tax act, individual/HUF not required to get his account audited paying the amount for carrying out any contractual work or professionals service in a financial year exceed 50,00,000 required to deduct TDS @ 5%. Now this details will be available in form 26as so that deductor can verify the amount form here. This credit is not available for claim in ITR by the buyer.

Part G: TDS defaults (processing of statements)

This seeks to reflect all the defaults in the respective TANs registered under your PAN. This will include the cases of short payment, short deduction, late payment of tax, late filing fee, etc. TDS defaults are liable for separate assessment proceedings and as such, it is always in your interest that this segment should always be clean and Nil.

PART H: Details of Turnover as per GSTR3B

This form of GSTR3B is updated in form 26as because a deductor can verify the turnover details directly from here. It includes GSTR Number, application Reference number, date of filling, return period, taxable turnover, and total turnover. It includes internal stock transfer data as well.

Important Notes for FORM 26AS

In PART C, Details of tax paid are displayed excluding TDS /TCS, Payment relating to security transaction tax, and banking cash transaction tax.Details of tax deducted at source in form 26as for form 15H/15H includes transactions for which declaration under section 197A has been Quoted

Details of SFT Transaction

How to view and download form 26as

STEP 1: First go to https://incometaxindiaefiling.gov.in and login with user id and password and captchaSTEP 2: Go to My Account and click on “view from 26AS” In the dropdown.STEP 3: Click on confirm and now you will be redirected to traces website.STEP 4: You are now on the traces website. Click the box on the screen and click on proceed.STEP 5: Click view tax credit to view 26as.STEP 6: Choose the assessment year and format in which you want to see 26as.If you want to see online, select the format as html otherwise in case of download you first have to view as HTML and click on download as Pdf.STEP 7: After the download, you can finally view 26AS.

Is it essential to view form 26AS before return Filing ?

Yes, it is very important to view this form before filing the return of income. Because it helps in claiming the tax credits and computation of income at the time of filing of return of income. Thus to avoid notice from the department, for easy processing of returns and speedy processing of refunds if any, this is required to be verified before filing the return of income.

Updation of form 26AS :

when TDS or TCS statements furnished by the deductors are uploaded to the TIN central system, challan information from the statements and the challan information from bank uploads are matched and Form 26AS is updated. Author: CA Rupali Agarwal Recommended Articles

Loans by the Directors to CompanyWhat is Franking ?Key man insurance policyHow to Pay TDS Online